CLP: Carbon Liquidity Pool

The Carbon Liquidity Pool (CLP) is a community-owned vault that provides liquidity to the Carbon Solver, the execution engine behind Carbon's decentralized perpetual exchange. CLP depositors earn yield from trading spreads and order flow generated by the platform, with hedged exposure that protects against directional market risk. Returns are backed by real trading revenue, not inflationary token emissions.

What Is the CLP?

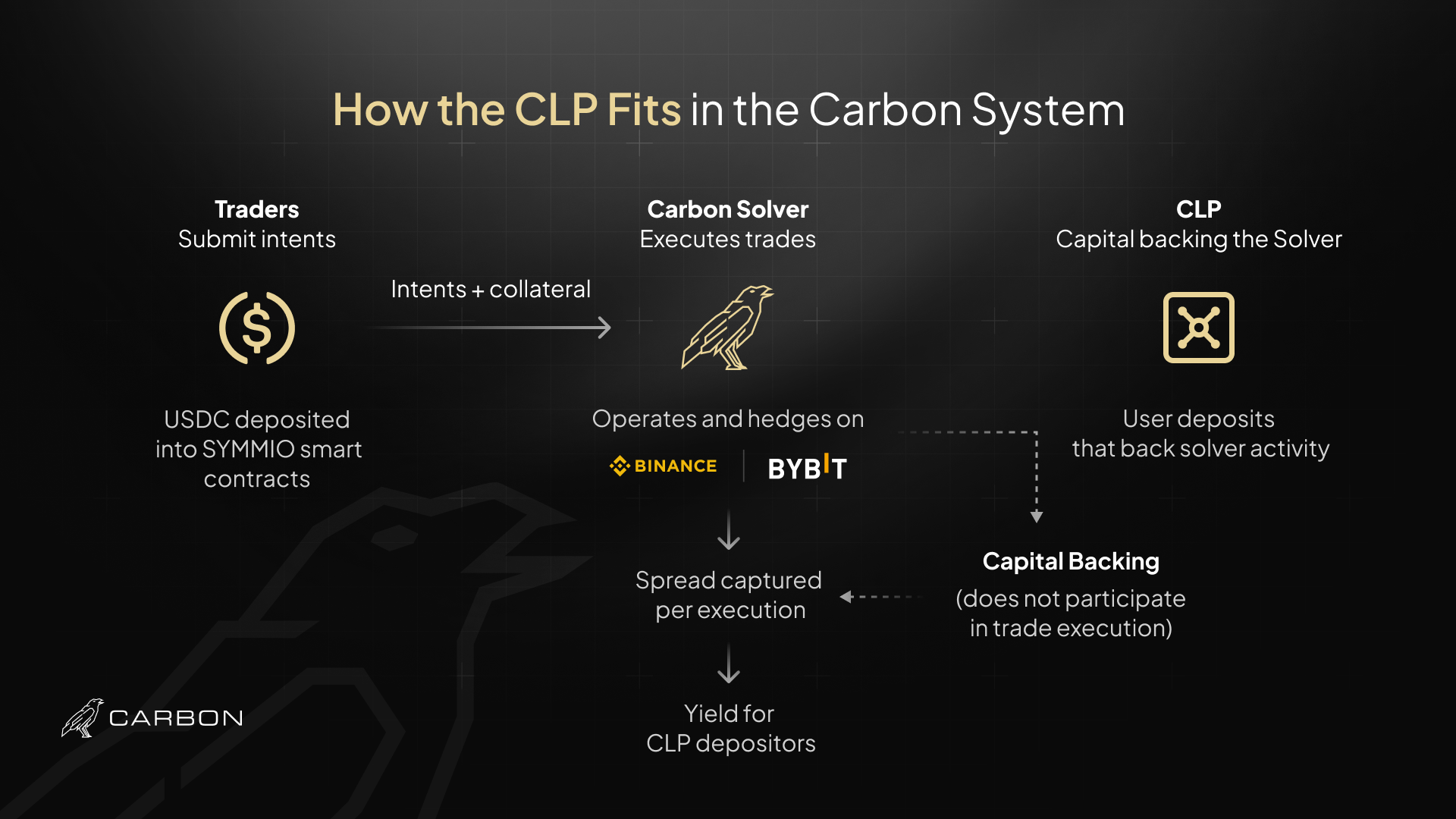

The Carbon Liquidity Pool is a structured vault that provides capital backing to the Carbon Solver — the professional market maker network that executes all trades on the Carbon platform. When a solver fills a trade on Carbon, they need collateral to support their bilateral position. The CLP provides part of that collateral. In return for this capital deployment, CLP depositors earn a share of the spreads and fees generated by every trade the solver executes.

This is not an LP pool in the AMM sense. CLP depositors are not acting as the direct counterparty for trader positions. They’re not taking on the full P&L risk of every trade that flows through the platform. Instead, the CLP is a structured capital vehicle where returns are tied to trading flow volume and spread capture, with deliberate risk management applied to limit directional exposure. The distinction matters. In GMX’s GLP pool, LPs are the literal counterparty for every trade. When traders make money, GLP loses it. When traders lose money, GLP gains it. The position is simple but exposes LPs to significant directional risk over time.

The CLP operates differently. The solver hedges positions on external venues, which means the directional exposure of the solver book is managed. CLP depositors benefit from the spread income generated by that activity without bearing the raw directional risk of an unhedged counterparty position.

How Returns Are Generated

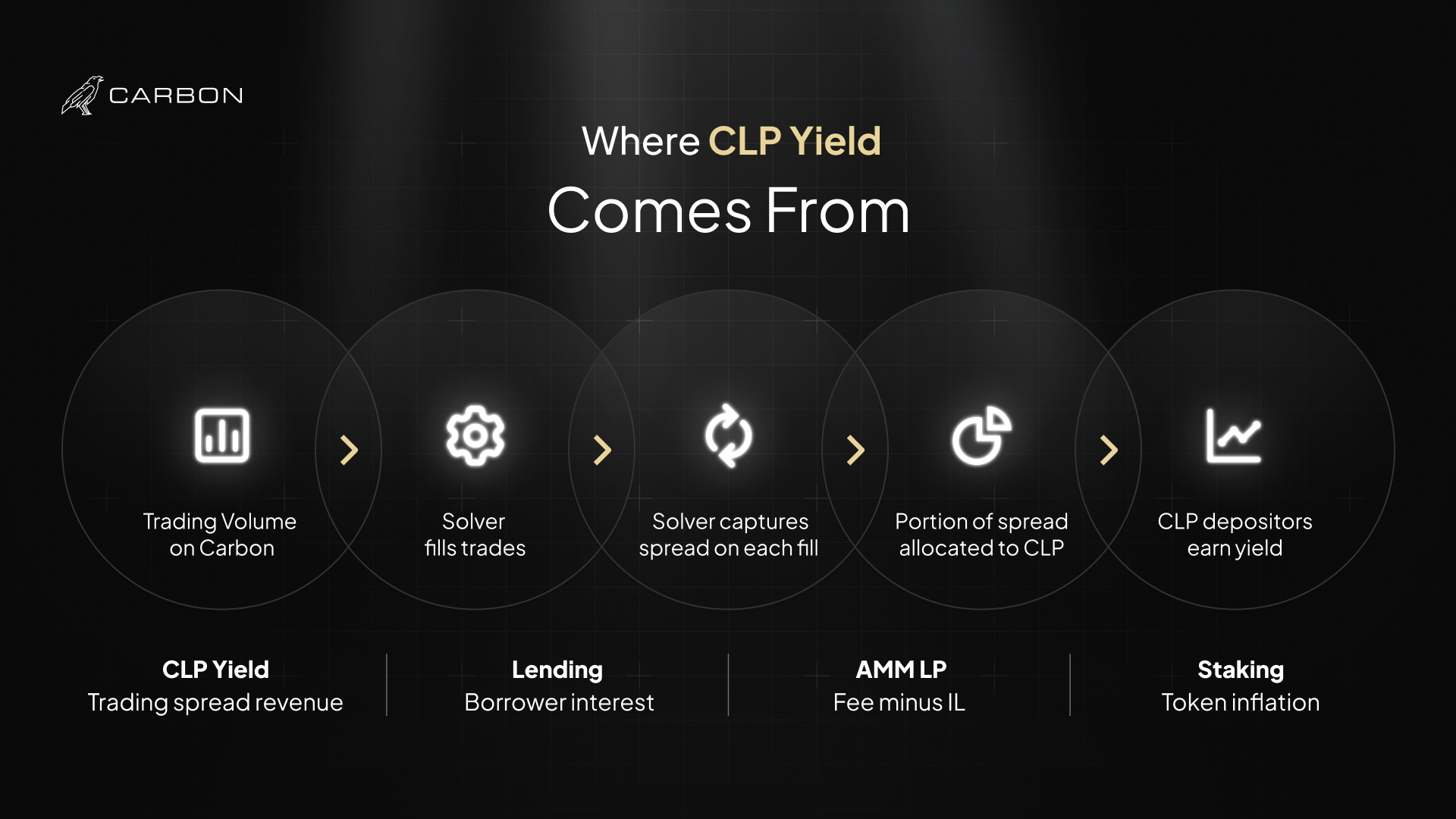

Every trade executed on Carbon generates spread income for the solver. The solver quotes at a price that includes their margin — the difference between what they charge the trader and what it costs to hedge their position on external venues. A portion of this spread income flows to the CLP based on the capital it contributes to the solver’s collateral backing.

Return depends on three factors: trading volume (more trades means more spread income), average spread captured per trade (tighter markets mean smaller spreads but typically higher volume), and the CLP’s share of total solver collateral.

This is fundamentally different from most DeFi yield sources.

Token emissions are inflationary rewards that dilute existing holders. The yield looks attractive until you account for the fact that the token you’re earning is also the token funding your rewards.

Lending yield fluctuates with borrower demand. During quiet markets, rates collapse toward zero. You’re paid by borrowers, and borrowers may not be there.

LP fees on AMMs compensate for impermanent loss. The net return after accounting for impermanent loss on volatile pairs is often negative, especially over extended periods.

CLP yield is a share of professional market making revenue from a live derivatives exchange. The same type of revenue that market making firms generate. The yield goes up when trading volume increases. It doesn’t depend on borrower demand, doesn’t involve impermanent loss, and isn’t funded by token inflation.

The Hedged Exposure Model

A central concern for any capital provider in a derivatives context is directional risk. If every trader on Carbon goes long ETH and ETH rises 20%, a naive counterparty pool would lose money proportional to the total long exposure.

Carbon’s solver model addresses this through mandatory hedging. When a solver fills a long ETH position, they must simultaneously hedge their exposure on external venues — immediately, as part of the fill. The SYMMIO protocol enforces this requirement through its collateral mechanics.

What this means for CLP depositors: the solver book is managed toward delta-neutral at any given time. The aggregate of all long and short positions on Carbon is offset by solver positions on external markets. The directional P&L of the solver book, and therefore the CLP’s exposure, is bounded.

This doesn’t mean zero risk. Timing risk exists — there is a brief window between a solver filling a trade and completing their hedge. Basis risk exists — the hedge may not perfectly offset if the hedging venue’s price temporarily differs from Carbon’s mark. Tail risk exists during extreme market dislocations where hedging itself becomes expensive or temporarily unavailable.

But the core directional risk that makes LP pool positions volatile — the risk of being the naked counterparty to a market that’s moving hard against you — is substantially mitigated by the mandatory hedging requirement built into the SYMMIO protocol.

How It Differs From Typical DeFi Yield

Most DeFi yield products are structurally different from the CLP. Understanding the difference matters before committing capital.

Lending protocols (Aave, Compound) pay you interest from borrowers. When demand is low — as it typically is during flat or bear markets — rates drop toward zero. The yield is real but variable and dependent on a third-party borrowing market.

AMM LP fees (Uniswap, Curve) are paid to compensate for the impermanent loss risk you take as an LP. On stable-stable pairs, this can work well. On volatile pairs, the net return after impermanent loss is frequently negative over extended holding periods. The fee income is real; the impermanent loss is real too.

Protocol staking rewards are typically funded by token inflation. New tokens are minted and distributed to stakers. This is yield in the accounting sense but it’s dilutive to all token holders. The “yield” is transferred from future holders to current stakers.

CLP yield is closer to being a passive investor in a market making operation than to any standard DeFi LP position. You’re providing capital to a professional operation and earning a share of what that operation generates from real trading activity. The comparison is to hedge fund LP returns or prime brokerage fee splits, not to AMM liquidity provision.

The yield is real because the trading activity is real. When volume goes up, returns go up. When volume is low, returns are lower. The driver is platform usage, not token economics.

How to Participate

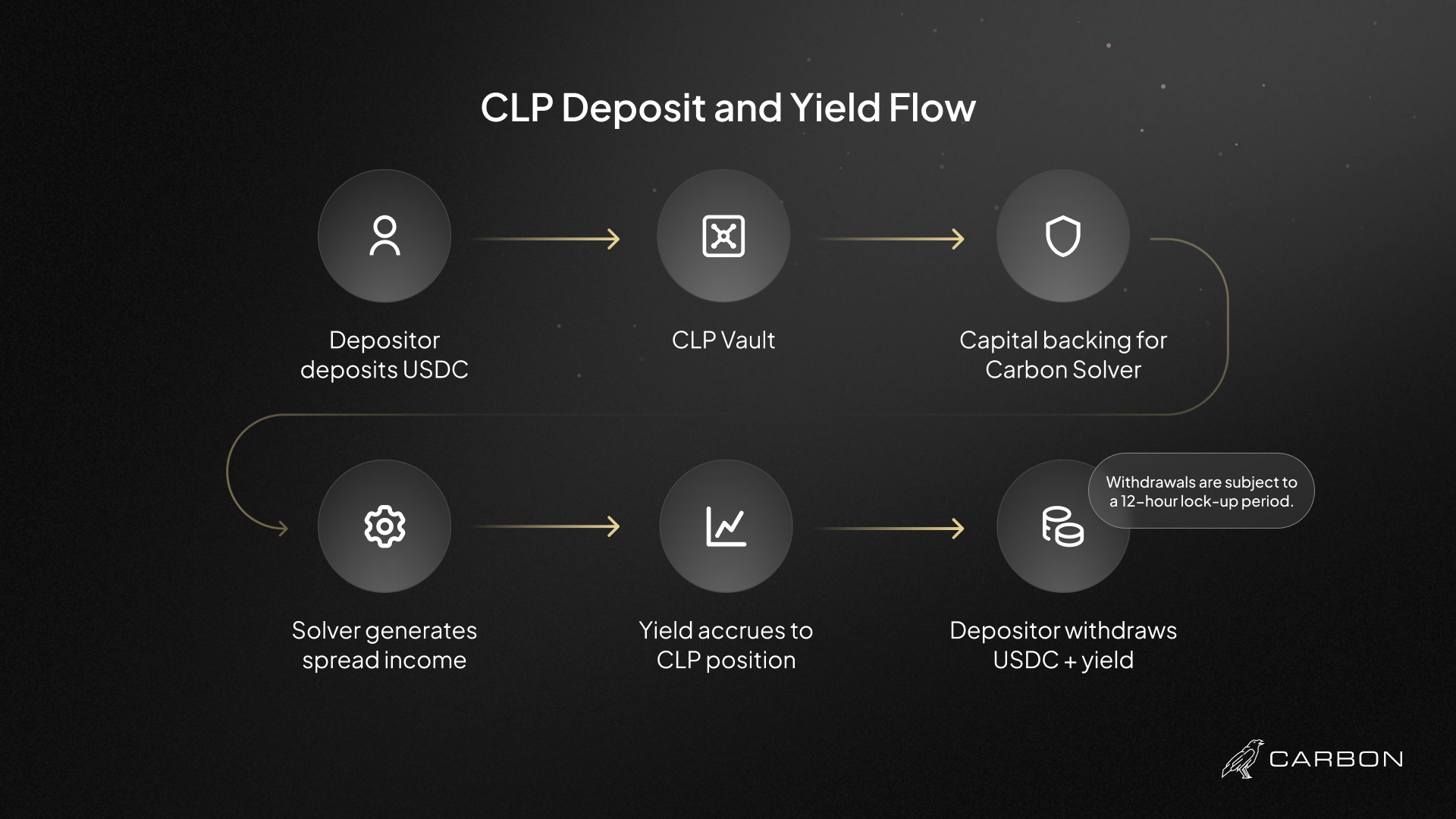

CLP participation works through a deposit mechanism available on the Carbon platform when the CLP launches.

You deposit USDC into the CLP vault. Your deposit is represented by a CLP position that tracks your proportional share of the total vault and its accrued yield. Yield accumulates continuously based on platform trading activity and is claimable at intervals specified at launch.

Specific deposit mechanics, minimum amounts, withdrawal lock periods, and fee structures will be documented in the CLP interface at launch. These parameters are designed to align the CLP’s capital base with the platform’s liquidity needs — the CLP works best with stable, longer-term capital rather than short-cycle in-and-out positions.

The CLP is intended for capital that can be deployed for sustained periods. Return profiles based on trading spread income compound over time as platform volume grows. This is not a short-term yield farming position.

Risk Factors

Honest risk disclosure is non-negotiable for a product where people are deploying capital. The following risks are real and should be understood before participating.

Smart contract risk. The CLP operates through smart contracts built on the SYMMIO protocol. Bugs in the code could lead to loss of funds. Carbon’s contracts are audited, but no audit eliminates all smart contract risk. This is the baseline risk of any DeFi position and should be accepted explicitly, not implicitly.

Solver liveness risk. The hedging model that protects CLP depositors depends on solvers functioning correctly and hedging on schedule. If solvers go offline, fail to hedge appropriately, or experience issues with their connected external venues, the CLP’s risk exposure increases. Carbon mitigates this through solver network redundancy and collateral requirements, but the dependency is real.

Basis and execution risk. The hedges solvers execute may not perfectly offset their on-chain exposure in real time. If hedging costs spike unexpectedly or hedge execution is poor, the spread captured by the solver — and therefore the yield flowing to CLP depositors — is compressed or negative.

Volume risk. CLP returns are tied to platform trading volume. During periods of low trading activity, returns will be lower than they are during high-volume periods. This is a feature of the structure, not a bug, but it means returns are variable.

Protocol governance risk. Parameters of the CLP — yield sharing ratios, withdrawal terms, solver collateral requirements — may change over time through governance decisions. Changes could affect the economics of the CLP position.

None of these risks are reasons not to participate. They are the risks inherent in providing capital to a market making operation. The expected return compensates for them. Depositors should size their CLP position according to their own risk tolerance and capital allocation framework, not according to the advertised APY alone.

The CLP is a specific bet: that Carbon’s trading volume will grow, that solver execution will remain high quality, and that spread income will produce meaningful returns relative to alternatives. If that bet is correct, CLP depositors earn real yield from real trading activity. That’s the honest description of what’s on offer.

Provide Liquidity

The CLP launches alongside Carbon’s full product release. In the meantime, explore Carbon’s trading platform.