Liquidity in DeFi Derivatives

Liquidity depth is the primary differentiator between on-chain derivatives platforms. While AMM-based DEXs are constrained by pool sizes and orderbook DEXs depend on on-chain market makers, solver-based exchanges like Carbon source executable liquidity from major centralized venues including Binance and Bybit through professional market makers who compete to fill orders. This model delivers CEX-grade depth on a decentralized platform without requiring users to give up custody of their funds.

The Liquidity Problem in On-chain Derivatives

The first question serious traders ask about any DeFi derivatives platform is: how deep is the book?

This is the right question. Liquidity depth determines whether you can open and close positions at the price you expect, at the size you need, without moving the market against yourself. A platform can have excellent UI, competitive fees, and an attractive token incentive program. None of it matters if the execution quality is poor.

The liquidity problem in on-chain derivatives has three dimensions.

Depth at size. For a $10,000 trade, almost any functional DEX will work. For a $500,000 trade on a less liquid pair, you need real depth. The difference between 2bps and 50bps of slippage at that size is the difference between a viable trading strategy and an unusable one. Most on-chain platforms perform acceptably at small sizes and badly at meaningful sizes.

Consistency across assets. Major DEXs can achieve reasonable depth on ETH and BTC. The depth on less liquid pairs — mid-cap crypto, equity CFDs, exotic forex — is a different story. Most liquidity models don’t scale across a wide asset universe without enormous capital commitments.

Depth under stress. During high-volatility events, LP pools can drain rapidly as arbitrageurs pick off stale prices. Market makers on orderbook platforms step back. Spread widens precisely when traders most need tight execution. The platforms that hold up during volatility are the ones traders trust long-term.

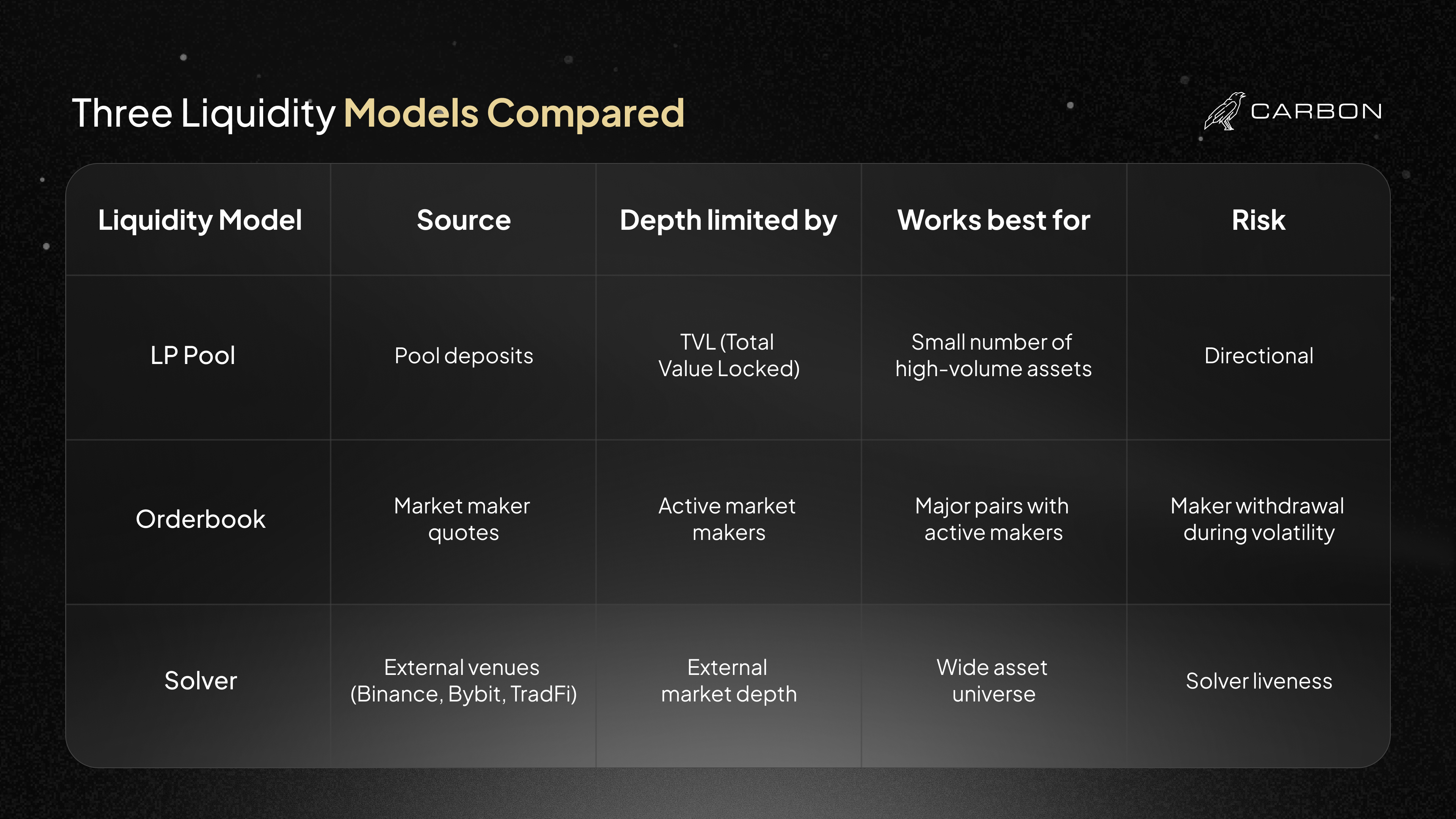

Three Models for On-chain Liquidity

On-chain derivatives platforms have converged on three distinct approaches to the liquidity problem. Each has real trade-offs.

LP Pool-Based Liquidity

GMX pioneered this model and proved it could work at scale. LPs deposit assets into a pool that acts as the collective counterparty for all trades on the platform. The pool earns fees on every trade. LPs take directional risk — when traders profit, the pool loses.

The advantage is simplicity and availability. No orderbook, no market maker dependency, no matching engine. The pool is always available as long as it has funds. LP-based platforms like GMX accumulated billions in TVL and demonstrated that DeFi derivatives could generate real fee revenue.

The constraint is economic. LP capital is expensive — providers require meaningful returns to accept directional risk, and those returns come from the traders on the other side. This limits how deeply pools can be funded on volatile or less liquid assets. Listing a new asset requires LPs to be willing to accept its directional risk. In practice, LP-based platforms work well on a handful of high-volume assets and struggle to maintain quality depth across a wide range.

On-chain Orderbooks

Hyperliquid and earlier dYdX represent this model. Market makers post resting bids and asks. Taker orders match against the book. Price discovery happens through competition between market makers, not through a formula.

When this model works well, it’s excellent. Hyperliquid has demonstrated CEX-quality execution on major pairs on a purpose-built L1. The on-chain orderbook model can achieve genuinely tight spreads with well-capitalized, active market makers.

The constraint is market maker behavior. Market makers are rational actors who widen spreads and reduce depth during high volatility — exactly when traders most need good execution. They can step back entirely from less liquid pairs when directional risk increases. And running a high-throughput orderbook on-chain requires purpose-built infrastructure, which is why the most successful orderbook DEXs have built their own chains rather than deploying on general-purpose L1s or L2s.

Solver Networks

Solver networks don’t pool capital or post resting orders. They route each trade to professional market makers who compete to fill it, sourcing their quotes from wherever the best liquidity exists externally.

For Carbon, that means Binance and Bybit for crypto markets, and institutional broker connections for equities, forex, and commodities. The solver fills the trade at the best available price from those external venues, then settles it on-chain. The depth is not on-chain. It’s in the external markets solvers are connected to.

How Carbon's Solver Model Solves the Problem

Carbon’s solver-based liquidity model addresses each dimension of the on-chain liquidity problem directly.

Depth at size. Carbon’s solver depth is bounded by the external markets solvers are connected to. For ETH, that means Binance’s ETH book. For Apple stock, that means NYSE equity markets. These are some of the deepest markets in the world. A $500,000 ETH trade on Carbon draws on the same depth that exists on Binance, not on the size of an on-chain pool.

Consistency across assets. Adding a new asset to a solver network doesn’t require dedicated capital deployment or pool creation. It requires that at least one solver in the network can hedge that asset. If a solver has access to an equity broker, they can quote equity CFDs. If a solver is connected to commodity markets, they can quote gold. The network’s asset coverage expands with solver connections, not with pool capital.

Depth under stress. When markets are volatile, Binance’s ETH book widens, but it doesn’t disappear. Solver quotes will reflect that — you’ll see wider spreads during extreme volatility — but the underlying market is still functioning and solvers can still hedge. This is more robust than LP pools, which can be drained, or orderbooks, which can see market makers step back entirely when directional risk spikes.

The Difference Between Quoted and Executable Depth

A common mistake when evaluating on-chain platforms is equating TVL or stated pool depth with actual execution quality.

TVL measures how much capital LPs have deposited. It doesn’t tell you what price impact you’ll get on a $200,000 trade. A $500M TVL pool with a standard AMM pricing curve can still have significant price impact on large trades because the curve, not the raw pool size, determines execution.

Orderbook depth charts show resting orders at this moment. They don’t show what the depth will be five seconds from now, after a market maker cancels their orders in response to a price movement.

The only reliable measure of execution quality is actual fill prices on real trades at various sizes across different market conditions. Slippage data at $10,000, $100,000, and $500,000 notional across different volatility environments tells you what a platform actually delivers. TVL tells you how much capital someone has committed. It doesn’t tell you what you’ll actually get.

Carbon’s solver model is designed to optimize for executable depth: the depth that actually executes when you submit a trade, not depth that evaporates under pressure. Because solvers hedge on external venues rather than posting capital in pools, their quoting ability is tied to the health of those external markets, which are larger and more robust than any on-chain alternative.

The Carbon Liquidity Pool Layer

The CLP (Carbon Liquidity Pool) adds a community capital layer on top of the solver network. CLP depositors provide collateral that the Carbon Solver uses as backing, earning yield from the trading spreads and order flow generated by the platform.

This is not an LP pool in the traditional AMM sense. CLP depositors don’t act as a collective counterparty for trades. They don’t bear the full directional risk of the trader order flow. Instead, the CLP provides capital that backs the solver’s positions, with hedged exposure that limits directional risk. Returns come from spread income and order flow, not from being the counterparty to every trade.

The result is that Carbon’s total liquidity capacity has two sources: solver liquidity sourced from external venues (Binance, Bybit, TradFi brokers), and CLP capital that provides additional collateral backing to the solver system. Both contribute to execution quality through different mechanisms.

For liquidity providers, the CLP offers a specific proposition: earn yield from real trading revenue — spreads and flow from actual market activity — with managed directional exposure, not inflationary token emissions.

Why Liquidity Determines Platform Survival

In derivatives markets, execution quality is the product. UI, fee structures, and token incentives are secondary. Traders are not loyal to platforms for their color scheme or their Discord. They follow execution quality.

A 5bps improvement in average fill quality across thousands of trades per month compounds into significant edge for systematic traders. Even for discretionary traders, large slippage events are memorable and they erode trust rapidly. Platforms that consistently deliver good execution retain traders. Platforms that don’t, don’t.

This is why the history of perp DEXs is a history of liquidity models. GMX grew because LP-based execution worked at scale. Hyperliquid attracted serious traders because its orderbook execution matched what they were used to on Binance. The platforms that failed generally failed because they couldn’t maintain execution quality as they scaled.

Carbon’s bet is that solver-based execution — sourcing liquidity from where it already exists in abundance, rather than trying to build comparable depth from scratch on-chain — is the model that holds up best as the platform scales across 550+ crypto pairs and 200+ RWA markets.

Execution quality is the bet. The solver model is the mechanism. External liquidity depth is the foundation.

Start Trading

Carbon’s solver-based execution is live for 550+ crypto perpetual pairs. Experience CEX-depth liquidity on a self-custodial, decentralized platform.